1

RMIT Classification: Trusted

BUSM 2565

Understanding the

Business

Environment

Topic 7: Markets

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

An overview of the topic of markets in the business environment. It covers key concepts such as market demand, the law of demand, demand elasticity, market supply, and the law of supply. The document also discusses price determination and factors that affect demand and supply. The content is suitable for university-level study in business, economics, or related fields. The document could be useful as study notes, lecture notes, or a summary for preparing exams, assignments, or essays on the topic of markets and the business environment.

Typology: Cheat Sheet

1 / 56

This page cannot be seen from the preview

Don't miss anything!

2

7.1. Market Demand 7.2. Demand Elasticity 7.3. Market Supply

4

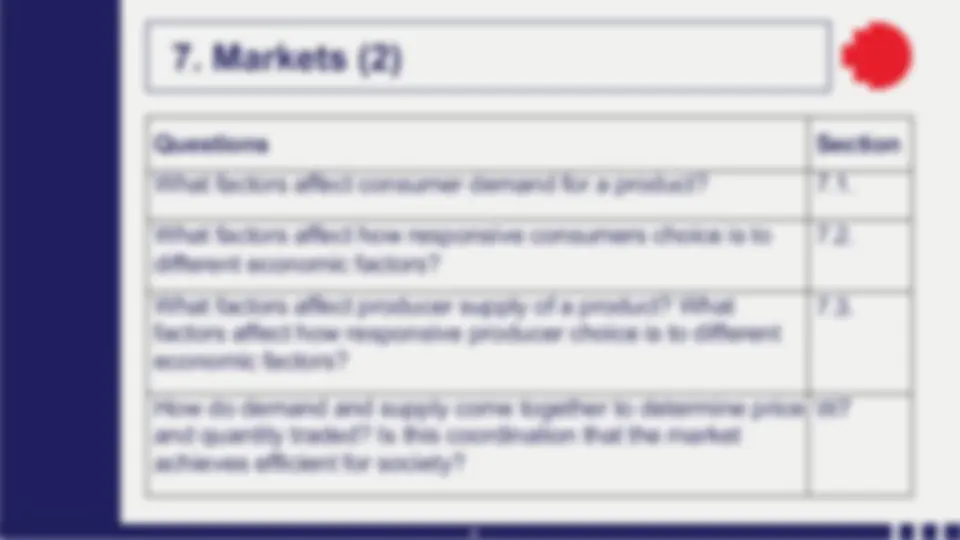

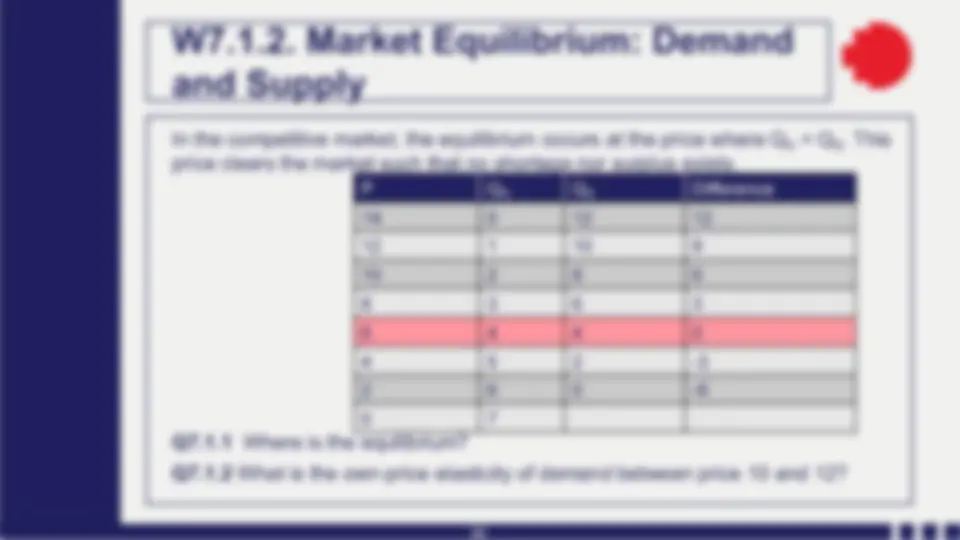

Questions Section What factors affect consumer demand for a product? 7.1. What factors affect how responsive consumers choice is to different economic factors?

What factors affect producer supply of a product? What factors affect how responsive producer choice is to different economic factors?

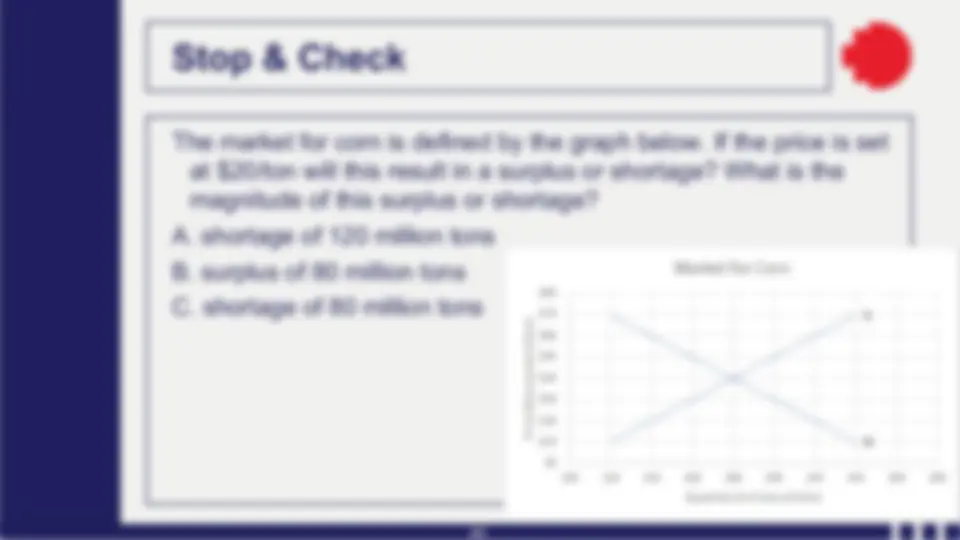

How do demand and supply come together to determine price and quantity traded? Is this coordination that the market achieves efficient for society?

5

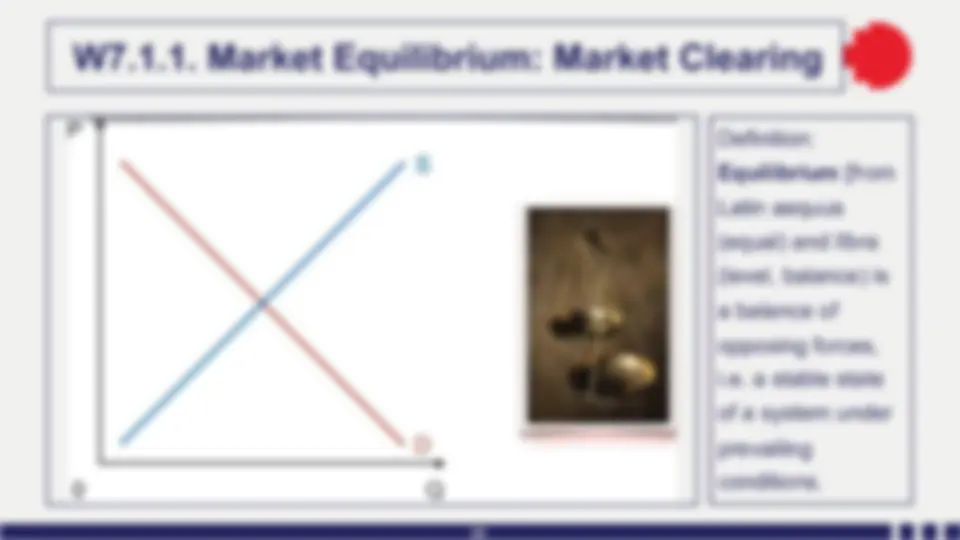

Definition: The market is an institution where the buyers and sellers of the same good or service come together to trade. The market model shows the relationship between two key variables, price and quantity, for both demand and supply. We analyse the model for equilibrium and efficiency.

7

Which of the following is not an assumption of the market model? a. competition is perfect b. prices are flexible c. people are perfectly informed d. resources are allocated perfectly efficiently

8

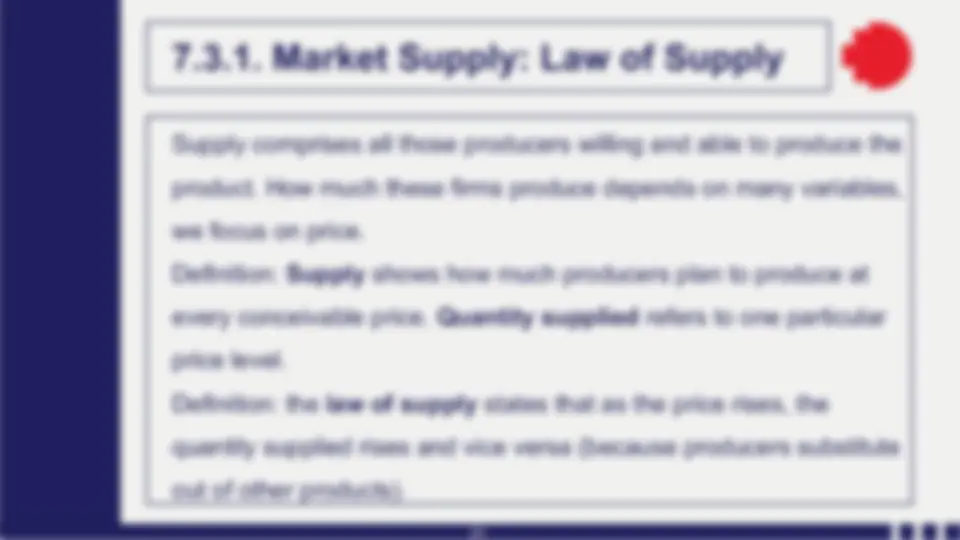

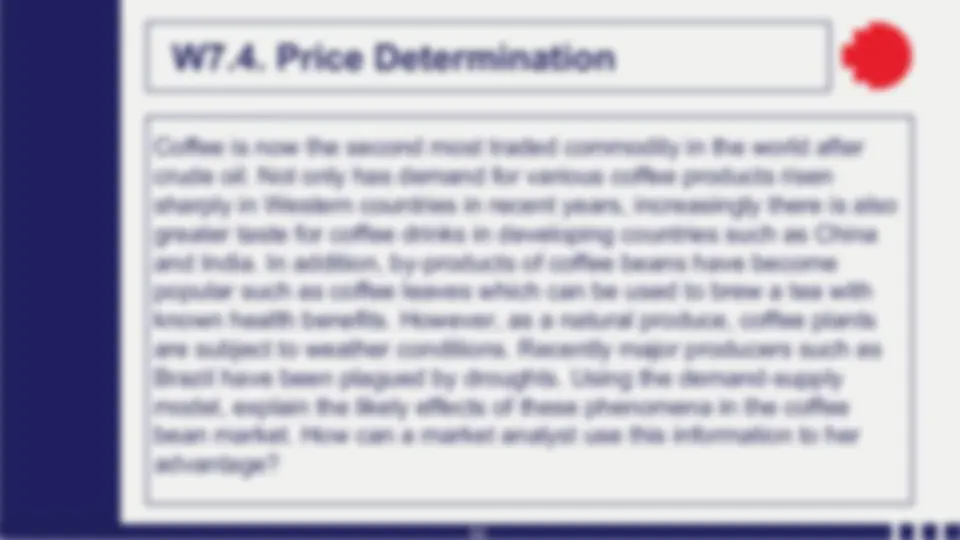

Demand comprises all those consumers willing and able to buy the product. How much people buy depends on many variables, we focus on price. Definition: Demand shows how much consumers plan to buy at every conceivable price. Quantity demanded (QD) refers to purchasing plans at one particular price (P). Definition: the law of demand states that as the price rises, the quantity demanded falls and vice versa (because consumers are relatively worse off and substitute into other products) while all other variables are held constant.

10

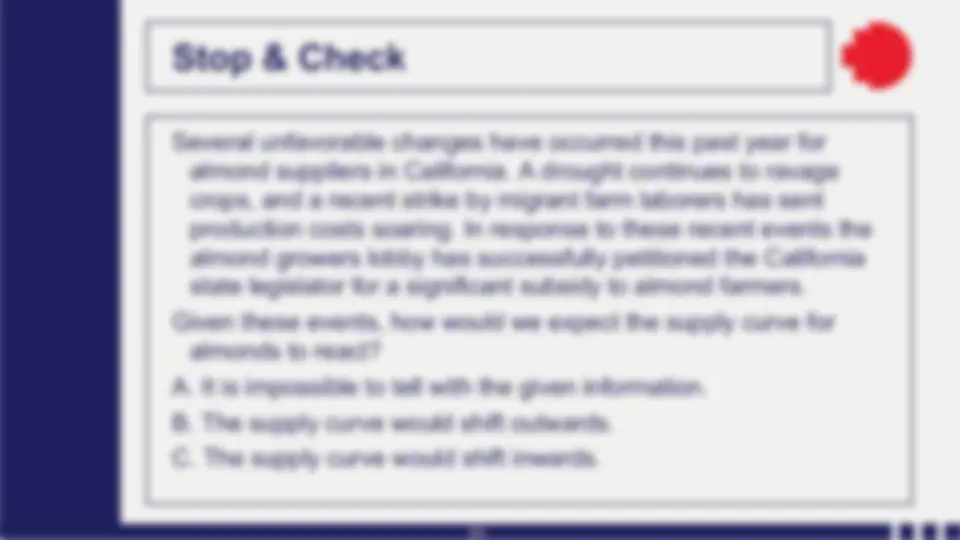

After Jamal increased the price of his trucks, he actually observed that his buyers increased rather than decreased their number of vehicle purchases. While he sold 16 trucks to his customers the month before the price increase, he sold a total of 18 trucks one month later. What is the most likely explanation for this apparent violation in the law of demand? A. Not all variables that affect demand have held constant this past month. For example, Jamal's customers' businesses have done exceptionally well this past month and so they are willing to buy more trucks despite the higher price. B. Economists need to rethink the law of demand, which has no way of accounting for this phenomenon. C. The law of demand does not apply to the market for trucks. As price increases, we would expect to see quantity demanded increase as well.

11

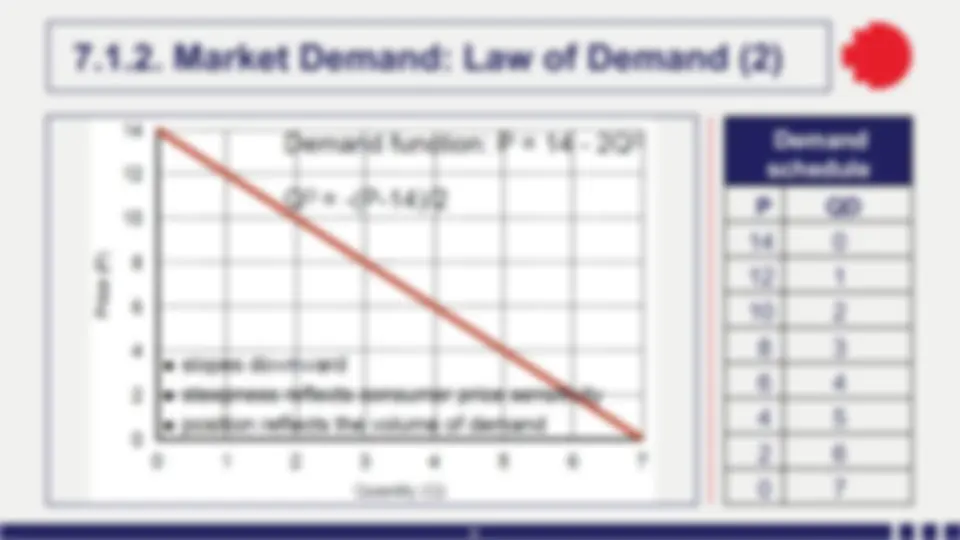

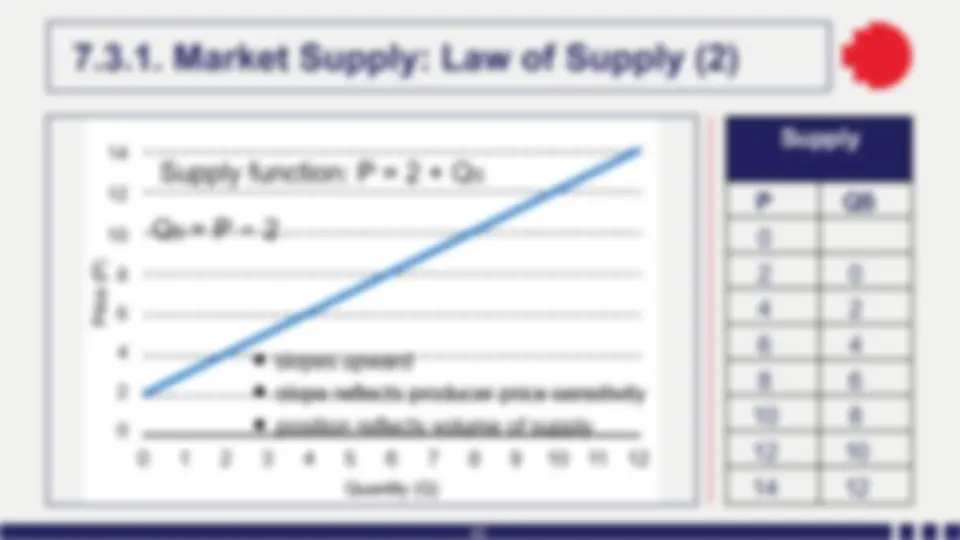

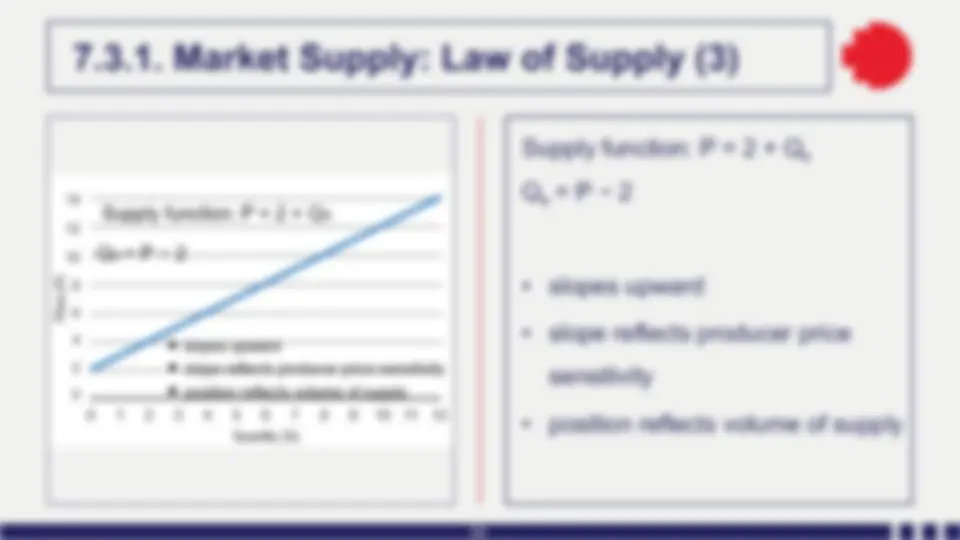

Demand function: P = 14 - 2 Q D Q D = - (P-14)/

13

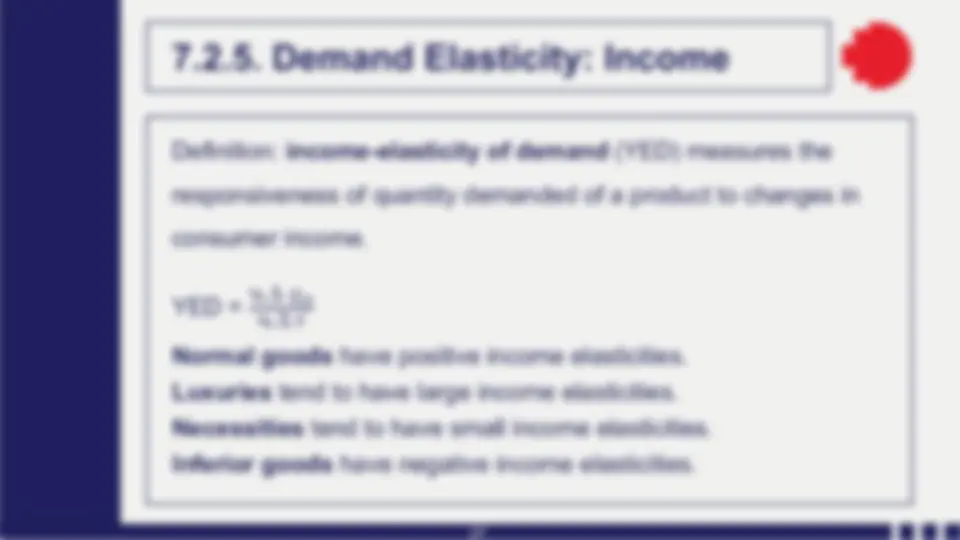

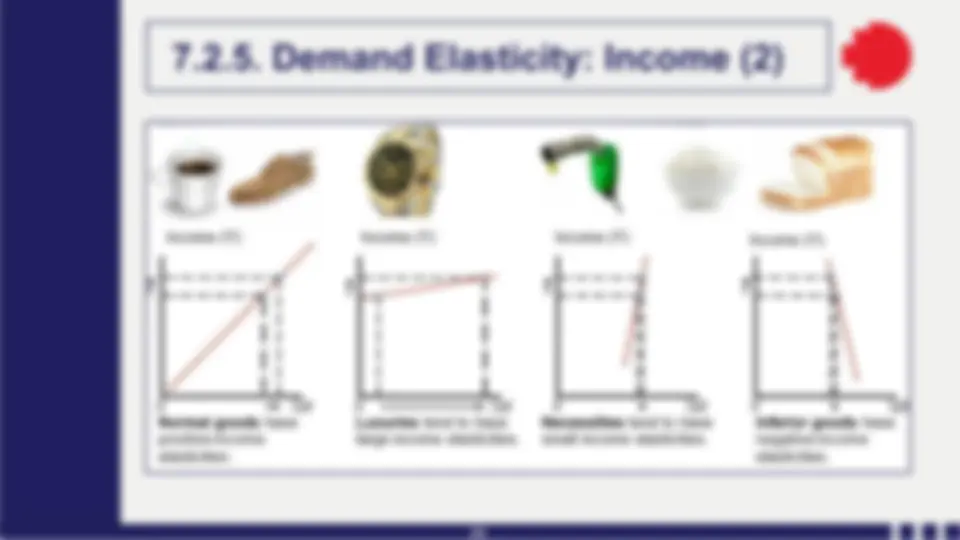

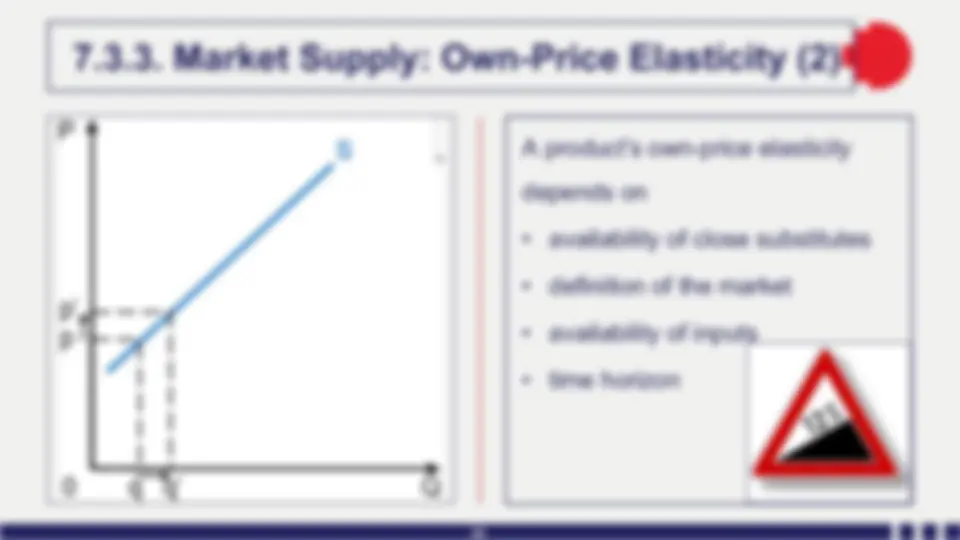

Definition: Elasticity measures the responsiveness of quantity to one of its determinants. We measure elasticity in the steepness (slope) of the curve concerned. There are many types of demand and supply elasticity to determinants such as price of this and related products, income etc. Definition: own-price elasticity of demand (PED) measures the responsiveness of quantity demanded of a product to its price. It reflects the sensitivity or responsiveness of consumer purchasing plans to price.

14

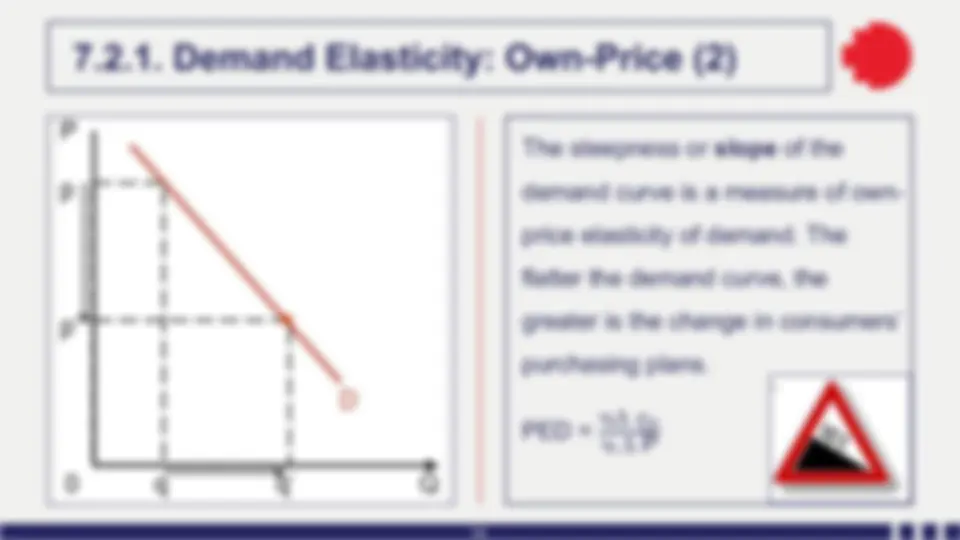

The steepness or slope of the demand curve is a measure of own- price elasticity of demand. The flatter the demand curve, the greater is the change in consumers’ purchasing plans. PED =

16

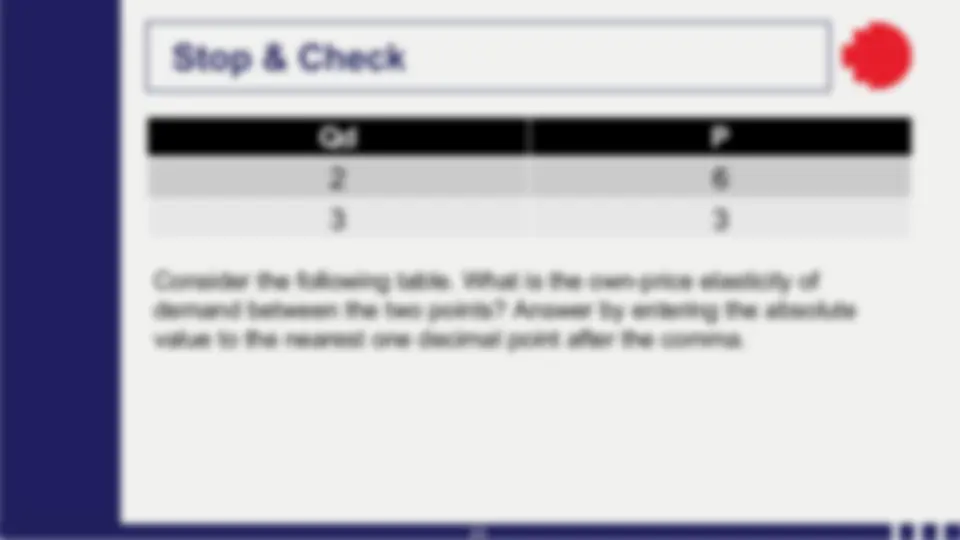

The measured elasticity between two given points of the demand curve depends on whether we calculate the change from the higher or the lower of the two values, e.g. from P=4 to P=10 or vice versa. As a result we can use the mid-point formula which gives the same result in either case: PED = ("" $ "#) (&" $ &#) x (&"' &#) ("" ' "#)

17

(( $)) (* $+,)

(*'+,) (('))

$.

+* /

()$() (+, $ *)

(+,'*) ()'()

$- .

+* /

The elasticity measured at different points of a linear curve differs because the percentage size of same absolute change (say a price fall of 4 either from 14 to 10 or 4 to 0) differs as we go along the axis. PED= ()$,) (+, $+*)

(+,'+*) ()',)

) $*

)* )

(/$() (,$*)

(,'*) (/'()

) $*

+)

19

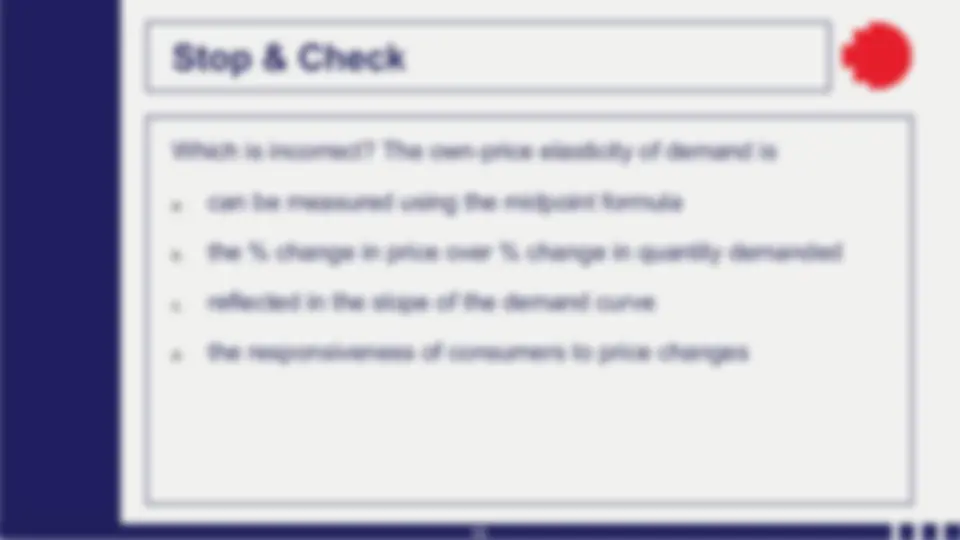

Which is incorrect? The own-price elasticity of demand is a. can be measured using the midpoint formula b. the % change in price over % change in quantity demanded c. reflected in the slope of the demand curve d. the responsiveness of consumers to price changes

20

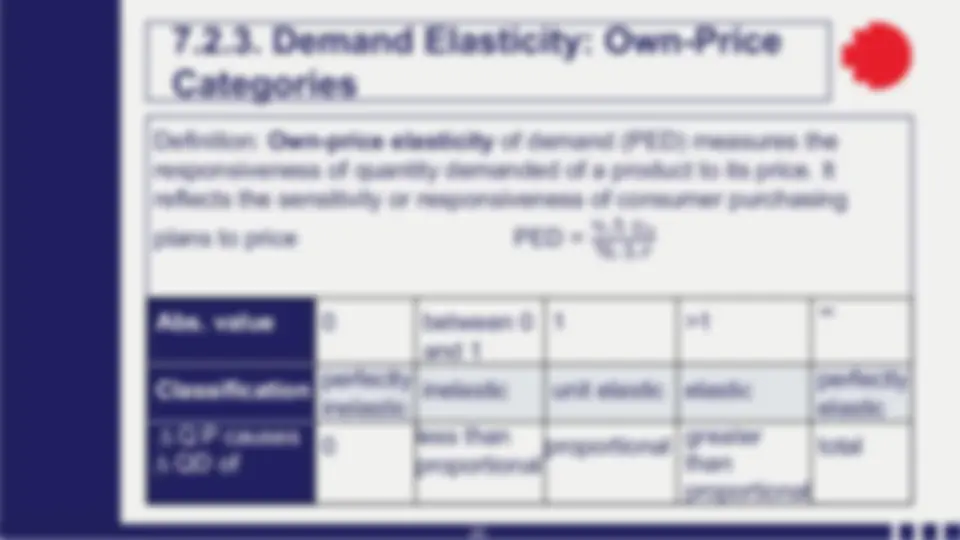

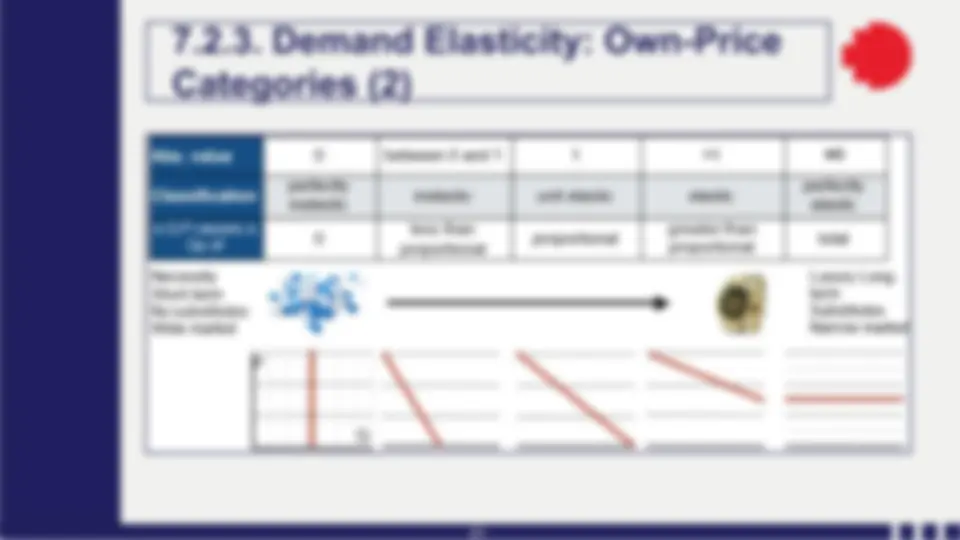

Definition: Own-price elasticity of demand (PED) measures the responsiveness of quantity demanded of a product to its price. It reflects the sensitivity or responsiveness of consumer purchasing plans to price PED =

Abs. value 0 between 0 and 1

Classification perfectly inelastic inelastic unit elastic elastic perfectly elastic ∆ Q P causes ∆ QD of

less than proportional proportional greater than proportional total