Download Stock Market Efficiency and Predictability of Stock Returns and more Lecture notes Finance in PDF only on Docsity!

The Efficient Market Hypothesis and Its Critics by Burton G. Malkiel, Princeton University CEPS Working Paper No. 91 April 2003

I wish to thank J. Bradford De Long, Timothy Taylor, and Michael Waldman for their extremelyhelpful observations. While they may not agree with all of the conclusions in this paper, they have strengthened my arguments in important ways.

The Efficient Market Hypothesis and Its Critics Burton G. Malkiel Abstract Revolutions often spawn counterrevolutions and the efficient market hypothesis in finance is no exception. The intellectual dominance of the efficient-market revolution has more been challenged by economists who stress psychological and behavioral elements of stock-price determination and by econometricians who argue that stock returns are, to a considerable extent, predictable. This survey examines the attacks on the efficient-market hypothesis and the relationship between predictability and efficiency. I conclude that our stock markets are more efficient and less predictable than many recent academic papers would have us believe.

The way I put it in my book, A Random Walk Down Wall Street , first published in 1973, a blindfolded chimpanzee throwing darts at the Wall Street Journal could select a portfolio that would do as well as the experts. Of course, the advice was not literally to throw darts but instead to throw a towel over the stock pages – that is, to buy a broad- based index fund that bought and held all the stocks in the market and that charged very low expenses. By the start of the twenty-first century, the intellectual dominance of the efficient market hypothesis had become far less universal. Many financial economists and statisticians began to believe that stock prices are at least partially predictable. A new breed of economists emphasized psychological and behavioral elements of stock-price determination, and came to believe that future stock prices are somewhat predictable on the basis of past stock price patterns as well as certain “fundamental” valuation metrics. Moreover, many of these economists were even making the far more controversial claim that these predictable patterns enable investors to earn excess risk-adjusted rates of return. This paper examines the attacks on the efficient market hypothesis and the belief that stock prices are partially predictable. While I make no attempt to present a complete survey of the purported regularities or anomalies in the stock market, I will describe the major statistical findings as well as their behavioral underpinnings, where relevant, and also examine the relationship between predictability and efficiency. I will also describe the major arguments of those who believe that markets are often irrational by analyzing the “crash of 1987,” the “Internet bubble” of the fin de siecle, and other specific irrationalities often mentioned by critics of efficiency. I conclude that our stock markets

are far more efficient and far less predictable than some recent academic papers would have us believe. Moreover, the evidence is overwhelming that whatever anomalous behavior of stock prices may exist, it does not create a portfolio trading opportunity that enables investors to earn extraordinary risk adjusted returns. At the outset, it is important to make clear what I mean by the term “efficiency”. I will use as a definition of efficient financial markets that they do not allow investors to earn above-average returns without accepting above-average risks. A well-known story tells of a finance professor and a student who come across a $100 bill lying on the ground. As the student stops to pick it up, the professor says, “Don’t bother—if it were really a $100 bill, it wouldn’t be there.” The story well illustrates what financial economists usually mean when they say markets are efficient. Markets can be efficient in this sense even if they sometimes make errors in valuation, as was certainly true during the 1999-early 2000 internet bubble. Markets can be efficient even if many market participants are quite irrational. Markets can be efficient even if stock prices exhibit greater volatility than can apparently be explained by fundamentals such as earnings and dividends. Many of us economists who believe in efficiency do so because we view markets as amazingly successful devices for reflecting new information rapidly and, for the most part, accurately. Above all, we believe that financial markets are efficient because they don’t allow investors to earn above-average risk-adjusted returns. In short, we believe that $100 bills are not lying around for the taking, either by the professional or the amateur investor. What I do not argue is that the market pricing is always perfect. After the fact, we know that markets have made egregious mistakes as I think occurred during the recent

them to reject the hypothesis that stock prices behave as random walks. There does seem to be some momentum in short-run stock prices. Moreover, Lo, Mamaysky and Wang (2000) also find, through the use of sophisticated nonparametric statistical techniques that can recognize patterns, some of the stock-price signals used by “technical analysts” such as “head and shoulders” formations and “double bottoms”, may actually have some modest predictive power. Economists and psychologists in the field of behavioral finance find such short- run momentum to be consistent with psychological feedback mechanisms. Individuals see a stock price rising and are drawn into the market in a kind of “bandwagon effect.” For example, Shiller (2000) describes the rise in the U.S. stock market during the late 1990s as the result of psychological contagion leading to irrational exuberance. The behavioralists offered another explanation for patterns of short-run momentum – a tendency for investors to underreact to new information. If the full impact of an important news announcement is only grasped over a period of time, stock prices will exhibit the positive serial correlation found by investigators. As behavioral finance became more prominent as a branch of the study of financial markets, momentum, as opposed to randomness, seemed reasonable to many investigators. However, there are several factors that should prevent us from interpreting the empirical results reported above as an indication that markets are inefficient. First, while the stock market may not be a mathematically perfect random walk, it is important to distinguish statistical significance from economic significance. The statistical dependencies giving rise to momentum are extremely small and are not likely to permit investors to realize excess returns. Anyone who pays transactions costs is unlikely to

fashion a trading strategy based on the kinds of momentum found in these studies that will beat a buy-and-hold strategy. Indeed, Odean (1999) suggests that momentum investors do not realize excess returns. Quite the opposite – a sample of such investors suggests that such traders did far worse than buy-and-hold investors even during a period where there was clear statistical evidence of positive momentum. This is so because of the large transactions costs involved in attempting to exploit whatever momentum exists. Similarly, David Lesmond, Michael Schill, and Chunsheng Zhou (2001) find that the transactions costs involved in undertaking standard “relative strength” strategies are not profitable because of the trading costs involved in their execution. Second, while behavioural hypotheses about bandwagon effects and underreaction to new information may sound plausible enough, the evidence that such effects occur systematically in the stock market is often rather thin. For example, Eugene Fama (1998) surveys the considerable body of empirical work on “event studies” that seeks to determine if stock prices respond efficiently to information. The “events” include such announcements as earnings surprises, stock splits, dividend actions, mergers, new exchange listings, and initial public offerings. Fama finds that apparent underreaction to information is about as common as overreaction, and post-event continuation of abnormal returns is as frequent as post-event reversals. He also shows that many of the return “anomalies” arise only in the context of some very particular model, and that the results tend to disappear when exposed to different models for expected “normal” returns, different methods to adjust for risk, and when different statistical approaches are used to measure them. For example, a study, which gives equal-weight to post-announcement returns of many stocks, can produce different results

Long-run Return Reversals In the short-run, when stock returns are measured over periods of days or weeks, the usual argument against market efficiency is that some positive serial correlation exists. But many studies have shown evidence of negative serial correlation – that is, return reversals -- over longer holding periods. For example, Fama and French (1988) found that 25 to 40 percent of the variation in long holding period returns can be predicted in terms of a negative correlation with past returns. Similarly, Poterba and Summers (1988) found substantial mean reversion in stock market returns at longer horizons. Some studies have attributed this forecastability to the tendency of stock market prices to “overreact.” DeBondt and Thaler (1995), for example, argue that investors are subject to waves of optimism and pessimism that cause prices to deviate systematically from their fundamental values and later to exhibit mean reversion. They suggest that such overreaction to past events is consistent with the behavioral decision theory of Kahneman and Tversky (1982), where investors are systematically overconfident in their ability to forecast either future stock prices or future corporate earnings. These findings give some support to investment techniques that rest on a “contrarian” strategy, that is, buying the stocks, or groups of stocks, that have been out of favor for long periods of time and avoiding those stocks that have had large run-ups over the last several years. There is indeed considerable support for long-run negative serial correlation in stock returns. However, the finding of mean reversion is not uniform across studies and is quite a bit weaker in some periods than it is for other periods. Indeed, the strongest empirical results come from periods including the Great Depression – which may be a

time with patterns that do not generalize well. Moreover, such return reversals for the market as a whole may be quite consistent with the efficient functioning of the market since they could result, in part, from the volatility of interest rates and the tendency of interest rates to be mean reverting. Since stock returns must rise or fall to be competitive with bond returns, there is a tendency when interest rates go up for prices of both bond and stocks to go down, and as interest rates go down for prices of bonds and stocks to go up. If interest rates mean revert over time, this pattern will tend to generate return reversals, or mean reversion, in a way that is quite consistent with the efficient functioning of markets. Moreover, it may not be possible to profit from the tendency for individual stocks to exhibit patterns of return reversals. Fluck, Malkiel and Quandt (1997) simulated a strategy of buying stocks over a 13-year period during the 1980s and early 1990s that had particularly poor returns over the past three to five years. They found that stocks with very low returns over the past three to five years had higher returns in the next period, and that stocks with very high returns over the past three to five years had lower returns in the next period. Thus, they confirmed the very strong statistical evidence of return reversals. However, they also found that returns in the next period were similar for both groups, so they could not confirm that a contrarian approach would yield higher-than- average returns. There was a statistically strong pattern of return reversal, but not one that implied an inefficiency in the market that would enable investors to make excess returns. Seasonal and Day-of-the-Week Patterns A number of researchers have found that January has been a very unusual month for stock market returns. Returns from an equally weighted stock index have tended to

market as a whole, have considerable predictive power. This section examines the body of work based on time-series analyses.

Predicting Future Returns from Initial Dividend Yields Formal statistical tests of the ability of dividend yields (that is, dividend-price ratios) to forecast future returns have been conducted by Fama and French (1988) and Campbell and Shiller (1988). Depending on the forecast horizon involved, as much as 40 percent of the variance of future returns for the stock market as a whole can be predicted on the basis of the initial dividend yield of the market index. An interesting way of presenting the results is shown in the top panel of Exhibit 1. The exhibit was produced by measuring the dividend yield of the broad U.S. stock market the Standard and Poor’s 500 Stock Index each quarter since 1926 and then calculating the market’s subsequent ten-year total return through the year 2000. The observations were then divided into deciles depending upon the level of the initial dividend yield. In general, the exhibit shows that investors have earned a higher rate of return from the stock market when they purchased a market basket of equities with an initial dividend yield that was relatively high, and relatively low future rates of return when stocks were purchased at low dividend yields. These findings are not necessarily inconsistent with efficiency. Dividend yields of stocks tend to be high when interest rates are high, and they tend to be low when interest rates are low. Consequently, the ability of initial yields to predict returns may simply reflect the adjustment of the stock market to general economic conditions. Moreover, the use of dividend yields to predict future returns has been ineffective since

the mid-1980s. Dividend yields have been at the three percent level or below continuously since the mid-1980s, indicating very low forecasted returns. In fact, for all 10 year periods from 1985 through 1992 that ended June 30, 2002, realized annual equity returns from the market index have averaged approximately 15 percent. One possible explanation is that the dividend behavior of U.S. corporations may have changed over time (See Bagwell and Shoven, 1989, and Fama and French, 2001). Companies in the twenty-first century may be more likely to institute a share repurchase program rather than increase their dividends. Thus, dividend yield may not be as meaningful as in the past as a useful predictor of future equity returns. Finally, it is worth noting that this phenomenon does not work consistently with individual stocks, as has been shown by Fluck, Malkiel and Quandt (1997). Investors who simply purchase a portfolio of individual stocks with the highest dividend yields in the market will not earn a particularly high rate of return. One popular implementation of such a “high dividend” strategy in the United States is the “Dogs of the Dow Strategy,” which involves buying the ten stocks in the Dow Jones Industrial Average with the highest dividend yields. For some past periods this strategy handily outpaced the overall average, and so several “Dogs of the Dow” mutual funds were brought to market and aggressively sold to individual investors. Such funds have generally underperformed the market averages during the 1995-99 period.

Predicting Market Returns from Initial Price-earnings Multiples The same kind of predictability for the market as a whole, as was demonstrated for dividends, has been shown for price-earnings ratios. The data are shown in the

Studies have found some amount of predictability of stock returns based on various financial statistics. For example, Fama and Schwert (1977) found that short-term interest rates were related to future stock returns. Campbell (1987) found that term structure of interest rates spreads contained useful information for forecasting stock returns, and Keim and Stambaugh (1986) found that risk spreads between high-yield corporate bonds and short rates had some predictive power. Again, even if some predictability exists, it may reflect time varying risk premiums and required rates of return for stock investors rather than an inefficiency. And it is far from clear that any of these results can be used to generate profitable trading strategies.

Cross-Sectional Predictable Patterns Based on Firm Characteristics and Valuation Parameters

A large number of patterns that are claimed to be predictable are based on firm characteristics and different valuation parameters.

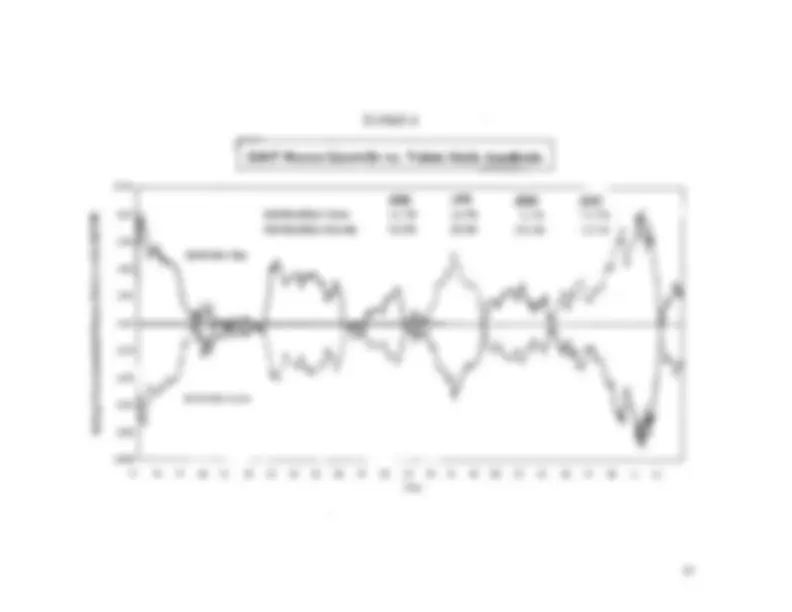

The Size Effect One of the strongest effects investigators have found is the tendency over long periods of time for smaller-company stocks to generate larger returns that those of large- company stocks. Since 1926, small-company stocks in the United States have produced rates of return over one percentage point larger than the returns from large stocks (Keim, 1983). Fama and French (1992) examined data from 1963 to 1990 and divided all stocks into deciles according to their size as measured by total capitalization. Decile one

contained the smallest ten percent of all stocks while decile ten contained the largest stocks. The results, plotted in Exhibit 2, show a clear tendency for the deciles made up of portfolios of smaller stocks to generate higher average monthly returns than deciles made up of larger stocks. The crucial issue here is the extent to which the higher returns of small companies represents a predictable pattern that will allow investors to generate excess risk-adjusted returns. According to the capital asset pricing model, the correct measure of risk for a stock is its “beta” – that is, the extent to which the return of the stock is correlated with the return for the market as a whole. If the “beta” measure of systematic risk from the capital asset pricing model is accepted as the correct risk measurement statistic, the size effect can be interpreted as indicating an anomaly and a market inefficiency, because using this measure portfolios consisting of smaller stocks have excess risk-adjusted returns. Fama and French point out, however, that the average relationship between “beta” and return during the 1963-1990 period was flat – not upward sloping as the capital asset pricing model predicts. Moreover, if stocks are divided up by beta deciles, ten portfolios constructed by size display the same kind of positive relationship shown in Exhibit 2. On the other hand, within size deciles, the relationship between beta and return continues to be flat. Fama and French suggest that size may be a far better proxy for risk than beta, and therefore that their findings should not be interpreted as indicating that markets are inefficient. Dependability of the size phenomenon is also open to question. From the mid- 1980s through the decade of the 1990s, there has been no gain from holding smaller stocks. Indeed, in most world markets, larger capitalization stocks produced larger rates

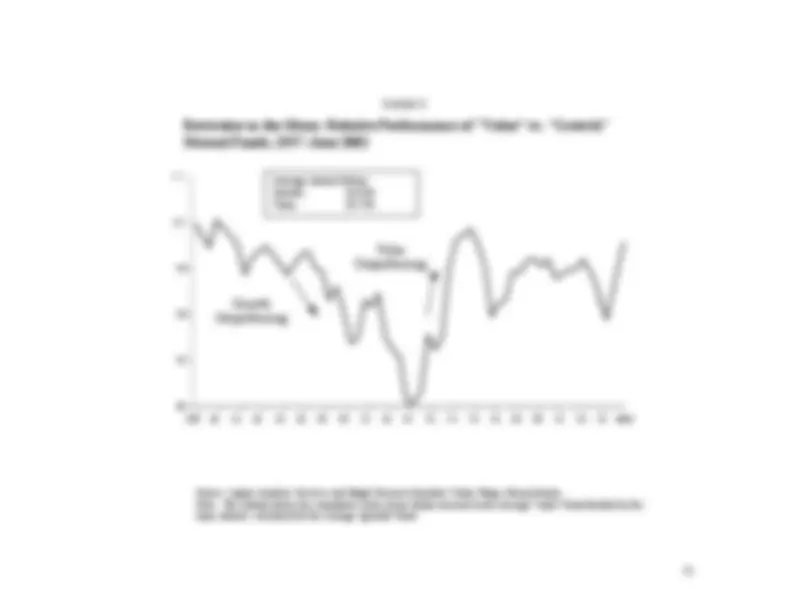

The ratio of stock price to book value, defined as the value of a firm’s assets minus its liabilities divided by the number of shares outstanding, has also been found to be a useful predictor of future security returns. Low price-to-book is considered to be another hallmark of so-called “value” in equity securities and is also consistent with the view of behavioralists that investors tend to overpay for “growth” stocks that subsequently fail to live up to expectations. Fama and French (1992) concluded that size and price-to-book-value together provide considerable explanatory power for future returns and once they are accounted for, little additional influence can be attributed to P/E multiples. Fama and French (1997) also conclude that the P/BV effect is important in many world stock markets other than the United States. Such results raise questions about the efficiency of the market if one accepts the capital asset pricing model, as Lakonishok, Schleifer and Vishny (1994) point out. But these findings do not necessarily imply inefficiency. They may simply indicate failure of the CAPM to capture all the dimensions of risk. For example, Fama and French (1993) suggest that the price-to-book value ratio may reflect another risk factor that is priced into the market and not captured by CAPM. Companies in some degree of financial distress, for example, are likely to sell at low prices relative to book values. Fama and French (1993) argue that a three-factor asset-pricing model (including price-to-book-value and size as measures of risk) is the appropriate benchmark against which anomalies should be measured. We also need to keep in mind that the results of published studies – even those done over decades – may still be time-dependent and ask whether the return patterns of academic studies can actually be generated with real money. Exhibit 3 presents average

actual returns generated by mutual funds classified by either their “growth” or “value” objectives. “Value” funds are so classified if they buy stocks with price-to-earnings and price-to-book-value multiples that are below the averages for the whole stock market. Over a period running back to the 1930s, it does not appear that investors could actually have realized higher rates of return from mutual funds specializing in “value” stocks. Indeed, the exhibit suggests that theFama-French period from the early 1960s through 1990 may have been a unique period in which value stocks rather consistently produced higher rates of return. Schwert (2001) points out that the investment firm of Dimensional Fund Advisors actually began a mutual fund that selected value stocks quantitatively according to the Fama and French (1993) criteria. The abnormal return of such a portfolio (adjusting for beta, the capital asset pricing model measure of risk) was a negative 0.2 percent per month over the 1993-1998 period. The absence during that period of an excess return to the “value” stocks is consistent with the results from “actively managed” value mutual funds shown in Exhibit 3.

The Equity Risk Premium Puzzle Another puzzle that is often used to suggest that markets are less than fully rational is the existence of a very large historical equity risk premium that seems inconsistent with the actual riskiness of common stocks as can be measured statistically. For example, using the Ibbotson data from 1926 through 2001, common stocks have produced rates of retain of approximately 10½ percent while high grade bonds have returned only about 5½ percent. I believe that this finding is simply the result of a