PATEROS TECHNOLOGICALCOLLEGE BSOA 1J

Bachelor of Science in Office Administration Principles of Accounting I

Reference: Basic Accounting" by Winlu Ballada Domdane Publishing

The Accounting Equation

The accounting equation is the most basic tool of accounting.

This equation represents the resources controlled by the enterprise, the present obligations of the enterprise and

the residual interest in the assets.

It states that assets must always equal liabilities and owner’s equity.

Assets = Liabilities + Owner’s Equity

Note that the assets are on the left side of the equation opposite the liabilities and owner’s equity. This explains

why increases and decreases in assets are recorded in the opposite manner (“mirror image”) as liabilities and

owner’s equity are recorded. The equation also explains why liabilities and owner’s equity follow the same rules of

debit and credit.

The logic of debiting and crediting is related to the accounting equation. Transactions may require additions to

both sides (left and right sides), subtractions from both sides, or an addition and subtraction on the same side, but

in all cases the equality must be maintained.

Debits and Credits – The Double-Entry System

Accounting is based on a double-entry system which means that the dual effects of a business transaction is

recorded. A debit side entry must have a corresponding credit side entry.

An account is debited when an amount is entered on the left side of the account and credited when an amount is

entered on the right side. The abbreviations for debit and credit are “Dr” from the Latin Debere and “Cr” from Latin

Credere, respectively.

The account type determines how increases or decreases in it are recorded. Increases in assets are recorded as

debits while decreases in assets are recorded as credit. Conversely, increases in liabilities and owner’s equity are

recorded by credits and decreases are entered as debits.

The rules of debit and credit for income and expense accounts are based on the relationship of these accounts to

owner’s equity. Income increases owner’s equity and expense decreases owner’s equity. Hence, increases in

income are recorded as credits and decreases as debits. Increases in expenses are recorded as debits and

decreases as credits. These are the rules of debit and credit.

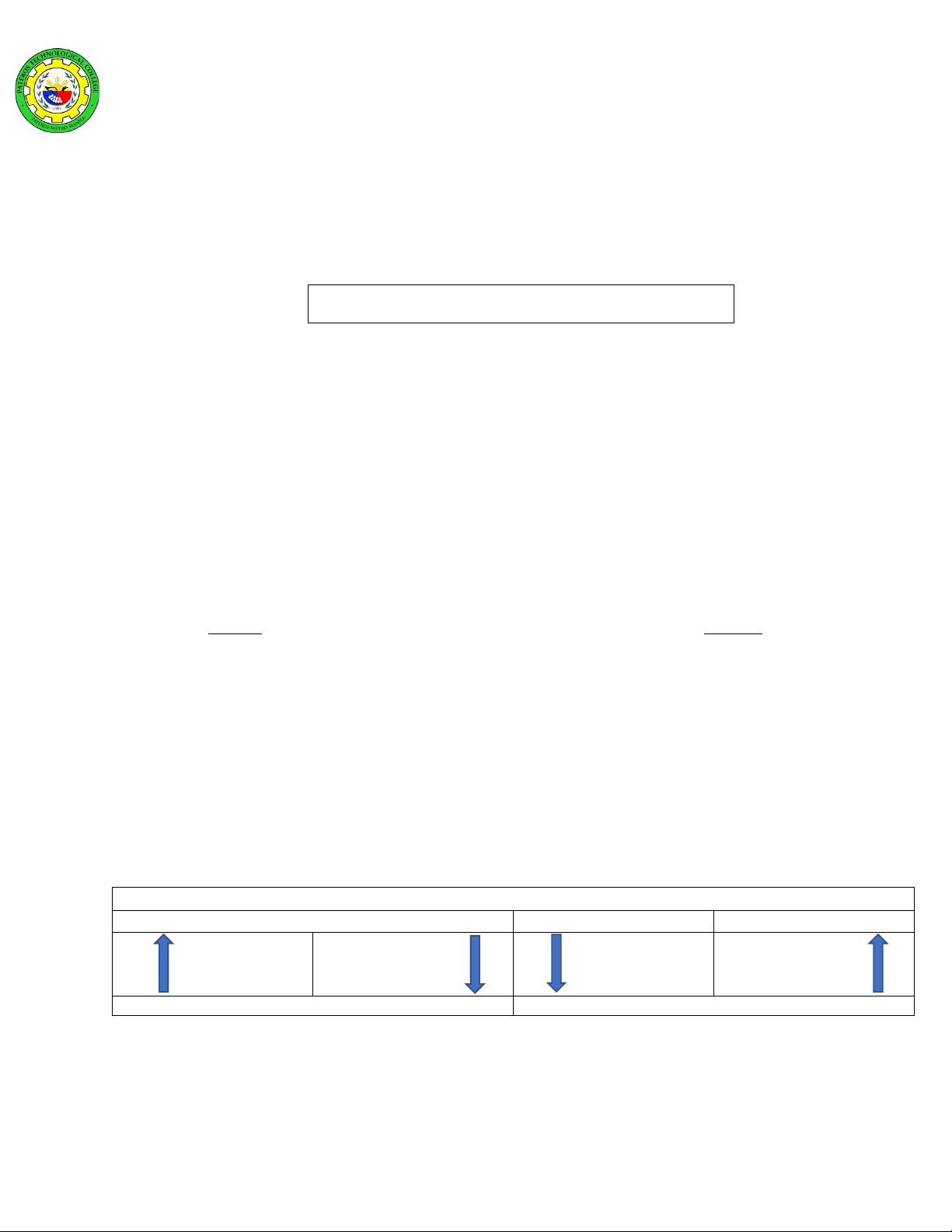

Balance Sheet Accounts

Assets

Liabilities

Owner’s Equity

Debit

Credit

Debit

Credit

(+)

(-)

(-)

(+)

Increases

Decreases

Decreases

Increases

Normal balance

Normal balance