Aswath Damodaran 1

Market Efficiency: Definitions and Tests

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

(c) In an efficient market, a strategy of minimizing trading, i.e., creating a portfolio and not trading unless cash was needed, would be superior to a ...

Typology: Lecture notes

1 / 40

This page cannot be seen from the preview

Don't miss anything!

l Question of whether markets are efficient, and if not, where the inefficiencies lie, is central to investment valuation. l If markets are, in fact, efficient, the market price is the best estimate of value , and the process of valuation becomes one of justifying the market price. l If markets are not efficient, the market price may deviate from the true value , and the process of valuation is directed towards obtaining a reasonable estimate of this value.

l Market 'inefficiencies'can provide the basis for screening the universe of stocks to come up with a sub-sample that is more likely to have under valued stocks l Saves time for the analyst l Increases the odds significantly of finding under and over valued stocks.

l The fact that the deviations from true value are random implies, in a rough sense, that there is an equal chance that stocks are under or over valued at any point in time, and that these deviationsare uncorrelated with any observable variable. For instance, in an efficient market, stocks with lower PE ratios should be no more or less likely to under valued than stocks with high PE ratios.

n If the deviations of market price from true value are random, it follows that no group of investors should be able to consistently find under or over valued stocks using any investment strategy.

l Definitions of market efficiency have to be specific not only about the market that is being considered but also the investor group that is covered. It is extremely unlikely that all markets are efficient to all investors , but it is entirely possible that a particular market (for instance, the New York Stock Exchange) is efficient with respect to the average investor. It is possible that some markets are efficient while others are not, and that a market is efficient with respect to some investors and not to others. This is a direct consequence of differential tax rates and transactions costs, which confer advantages on some investors relative to others.

l Definitions of market efficiency are also linked up with assumptions about what information is available to investors and reflected in the price. For instance, a strict definition of market efficiency that assumes that all information, public as well as private, is reflected in market prices would imply that even investors with precise inside information will be unable to beat the market.

l No group of investors should be able to consistently beat the market using a common investment strategy.

l An efficient market would also carry very negative implications for many investment strategies and actions that are taken for granted - (a) In an efficient market, equity research and valuation would be a costly task that provided no benefits. The odds of finding an undervalued stock should be random (50/50). At best, the benefits from information collection and equity research would cover the costs of doing the research. (b) In an efficient market, a strategy of randomly diversifying across stocks or indexing to the market, carrying little or no information cost and minimal execution costs, would be superior to any other strategy , that created larger information and execution costs. There would be no value added by portfolio managers and investment strategists. (c) In an efficient market, a strategy of minimizing trading , i.e., creating a portfolio and not trading unless cash was needed, would be superior to a strategy that required frequent trading.

n An efficient market does not imply that -

(a) stock prices cannot deviate from true value ; in fact, there can be large deviations from true value. The deviations do have to be random. (b) no investor will 'beat' the market in any time period. To the contrary, approximately half of all investors, prior to transactions costs, should beat the market in any period. (c) no group of investors will beat the market in the long term. Given the number of investors in financial markets, the laws of probability would suggest that a fairly large number are going to beat the market consistently over long periods, not because of their investment strategies but because they are lucky.

n In an efficient market, the expected returns from any investment will be consistent with the risk of that investment over the long term, though there may be deviations from these expected returns in the short term.

n There is an internal contradiction in claiming that there is no possibility of beating the market in an efficient market and then requiring profit-maximizing investors to constantly seek out ways of beating the market and thus making it efficient. n If markets were, in fact, efficient, investors would stop looking for inefficiencies , which would lead to markets becoming inefficient again. n It makes sense to think about an efficient market as a self-correcting mechanism , where inefficiencies appear at regular intervals

n Proposition 1: The probability of finding inefficiencies in an asset market decreases as the ease of trading on the asset increases. To the extent that investors have difficulty trading on an asset, either because open markets do not exist or there are significant barriers to trading, inefficiencies in pricing can continue for long periods.

n Corollary 1: Investors who can estabish a cost advantage (either in information collection or transactions costs) will be more able to exploit small inefficiencies than other investors who do not possess this advantage.

n Establishing a cost advantage, especially in relation to information, may be able to generate excess returns on the basis of these advantages. Thus a John Templeton, who started investing in Japanese and othe Asian markets well before other portfolio managers, might have been able to exploit the informational advantages he had over his peers to make excess returns on his portfolio.

n Proposition 3: The speed with which an inefficiency is resolved will be directly related to how easily the scheme to exploit the inefficiency can be replicated by other investors. The ease with which a scheme can be replicated itself is inversely related to the time, resources and information needed to execute it. Since very few investors single-handedly possess the resources to eliminate an inefficiency through trading, it is much more likely that an inefficiency will disappear quickly if the scheme used to exploit the inefficiency is transparent and can be copied by other investors.

n An event study is designed to examine market reactions to, and excess returns around specific information events. The information events can be market-wide, such as macro-economic announcements, or firm-specific, such as earnings or dividend announcements.

l Step 1: Identify the event

(1) The event to be studied is clearly identified, and the date on which the event was announced pinpointed. Announcement Date

___________________________________|________________________

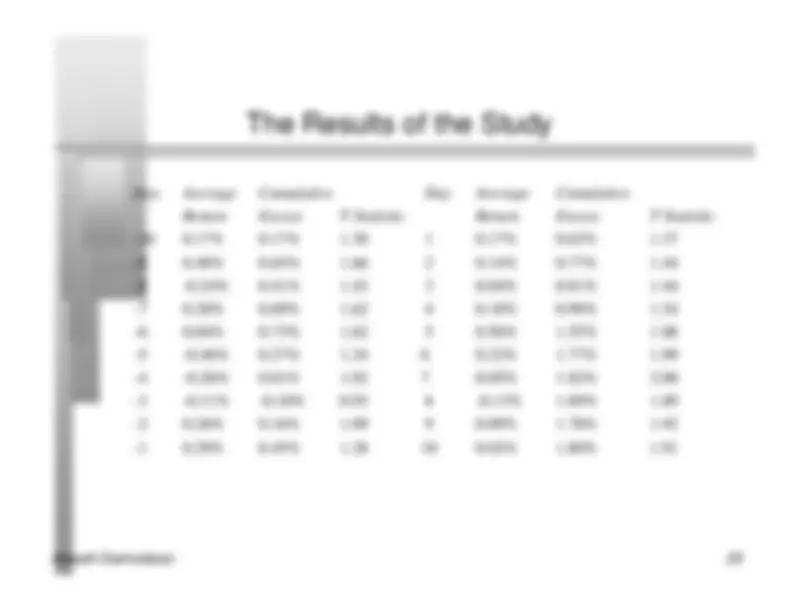

n The returns, by period, around the announcement date, are adjusted for market performance and risk to arrive at excess returns for each firm in the sample. For instance, if the capital asset pricing model is used to control for risk - Excess Return on day t = Return on day t - Beta * Return on market on day t ER-jn ................. ERj0 ..................ER+jn

_______|_______________________|________________________|____

Return window: -n to +n

Where ER = Excess return on stock j in period t

n The excess returns, by day, are averaged across all firms in the sample and a standard error is computed. Average excess return on day t=

where,

N = Number of events in the event study

ERjt j = 1 N

j= N