Download Know the ccf a. Long-term nib and more Summaries Mathematics in PDF only on Docsity!

Jdksgdasx,sbj

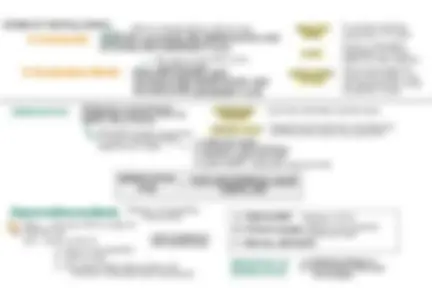

Items of Other comprehensive income

1. UG/L FROM FVOCi

DEBT SECURiTY

EQUiTY SECURiTY

2. CHANGES iN FV ATTRiBUTED TO CREDiT RiSK OF FVTPL

3. REVALUATiON SURPLUS (PPE)

4. REMEASUREMENT OF DEFiNED BENEFiT PLAN

5. GAiN/LOSS ON TRANSLATiON OF FOREiGN OPERATiON

6. UG/L FROM DERiVATiVES DESiGNATED AS CASH FLOW HEDGE

RECLASSiFiCATiON

ADJUSTMENTS

(CHARGED TO P/L)

NOT SUBJ TO

RECLASSiFiCATiON

(RETAiNED EARNiNGS)

✓ ✓ ✓ ✓ ✓ ✓ ✓

COMPREHENSiVE iNCOME = NET iNCOME + OTHER COMPREHENSiVE iNCOME

OCI

BEG BAL

CHANGES FOR

THE PERiOD

SCI

SCE

SCE

SFP (EQUiTY SiDE)

RETAiNED EARNiNGS

BEG BAL

NET iNCOME

PRiOR PERiOD ERRORS

CHANGES iN ACCTG

POLiCY

ENDiNG BAL

DiViDENDS

ENDiNG BAL

Retrospective

restatement

(±) APPROPRiATED UNAPPROPRiATED RESTRiCTED UNRESTRiCTED

Jdksgdasx,sbj

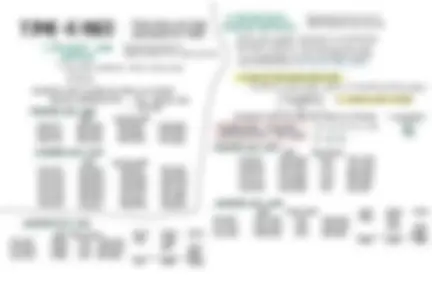

Balance sheet perspective

ASSETS

LiABiLiTiES

EQUiTY

CURRENT

NON-CURRENT

OPERATiNG

CURRENT

NON-CURRENT

INVESTiNG

OPERATiNG

FiNANCiNG

FiNANCiNG

INTEREST RECEiVED

INTEREST PAiD

DiViDENDS RECEiVED

DiViDENDS PAiD

OPERATiNG

OPERATiNG

OPERATiNG

FiNANCiNG

INVESTiNG

FiNANCiNG

INVESTiNG

OPERATiNG

Benchmark Alternative

Net cash from:

operating activities xx

Investing activities xx

financing activities xx

Net cash increase (decrease) Pxx

Add: cash & ce, beg xx

Cash & CE, ending Pxx

Direct method:

Cash received from customers xx Cash paid to suppliers (xx) Cash paid to operating expenses (xx) Separately presented: Interest paid (xx) Income tax paid (xx) Net cash provided (used) OA xx

Indirect method:

Income before tax

- Adjustments for non-cash items

- dep’n expense

- amort’n expense

- Changes in working capital

- Separately presented: Interest paid Income tax payable Indirect rel Direct rel

Jdksgdasx,sbj

EiTHER OF THE FOLLOWiNG:

COST LESS ACCUMULATED DEPRECiATiON AND

ACCUMULATED iMPAiRMENT LOSS

A. Cost model B. Revaluation Model REVALUED AMOUNT LESS

ACCUMULATED DEPRECiATiON AND

ACCUMULATED iMPAiRMENT LOSS

Will not change almost all the time.

Fair value of the PPE on the

revaluation date

PER CLASS

BASiS

To prevent selective

application of model

Cost or revaluation

regardless of choice

made for other classes.

CLASS

ASSETS WiTHiN A CLASS

All are accounted for

using cost model or all

are accounted for using

revaluation model

SYSTEMATiC ALLOCATiON OF DEPRECiABLE AMOUNT OVER THE USEFUL LiFE OF THE PPE DEPRECiABLE Cost less estimated residual value AMOUNT Expected proceeds from the disposal Expected number of periods^ RESiDUAL VALUE of PPE at the end of its useful life. or output that the PPE is usable by an entity.

DEPRECiATiON

A. EXPECTED USAGE

B. TECHNiCAL OBSOLESCENCE C. PHYSiCAL WEAR AND TEAR D. LEGAL LiMiTS (^) Leasehold improvements

DEPRECiATiON

RATE

COST LESS RESIDUAL VALUE

= USEFUL LIFE

Depreciation methods (^) A. TiME-BASED Manner of computing depreciation

B. OUTPUT-BASED

C. SPECiAL METHODS

Start - when the PPE is ready for intended use End - earlier of the ff: a. Date of derecognition b. Held for sale c. Fully depreciated (depreciation will continue if Residual value decreases) LAND iS NORMALLY NON-DEPRECiABLE Passage of time Based on the quantity produced/used

REPORTiNG OF

DEPRECiATiON

A. EXPENSED GENERALLY

B. CAPiTALiZED iN THE COST OF AN ASSET 0

Jdksgdasx,sbj

FUNCTiON OF TiME

Time-based (PASSAGE OF TiME)

1. STRAiGHT - LiNE

METHOD

2. DECREASiNG -

CHARGE METHODS

Equal amounts of

depreciation for each period

Benefits realized = same every year

Building A. SUM-OF-THE-YEARS-DIGIT (SYD)

Decreasing amount of

depreciation per period

PPEs with sudden decrease in productivity

Benefits realized = decreasing every year

To compensate for the increased repairs

and maintenance during the later years.

EXAMPLE: COST 1M, RES VAL 100K, UL 5 YEARS

ANNUAL DEPRECiATiON = (1M - 100K)/5 YRS = 180, DEP ACCUM DEP 12/31/21 180,000 180,000 820, 12/31/22 180,000 360,000 640, 12/31/23 180,000 540,000 (^) 460, ACQUiRED JULY 1, 2021 DEP ACCUM DEP 12/31/21 90,000 90,000 910, 12/31/22 180,000 270,000 730, 12/31/23 180,000 450,000 550, 12/31/24 180,000 630,000 370, 12/31/25 180,000 810,000 190, 12/31/26 90,000 900,000 100,

= [ N X (N+1) ]

ACQUiRED OCT 1, 2021

Fraction of the years’ digit in computing depreciation

N = USEFUL LiFE iN YEARS EXAMPLE: COST 1M, RES VAL 100K, UL 5 YEARS = [ 5 X (5+1) ] 5 + 4 + 3 + 2 + 1 = 15 2 NUMERATOR > CHANGES DENOMiNATOR > THE SAME = 15 Y1 Y2 Y DEP FRACTiON 12/31/21 900,000 5/15 300, 12/31/22 900,000 4/15 240, 12/31/23 900,000 3/15 180, 12/31/24 900,000 2/15 120, 12/31/25 900,000 1/15 60, ACQUiRED JULY 1, 2021 ACQUiRED JAN 1, 2021 DEP FRACTiON 12/31/21 900,000 5/15 300, 12/31/22 900,000 4/15 240, 12/31/23 900,000 3/15 180,

150K 150K

120K 120K

90K

150K 270K 210K

DEP FRACTiON 12/31/21 900K 5/15 300, 12/31/22 900K 4/15 240, 12/31/23 900K 3/15 180,

75K 225K

60K 180K

45K

75K 285K 225K

ACQUiRED JAN 1, 2021 .

Jdksgdasx,sbj

Special depreciation methods

- COMPOSiTE METHOD

1. GROUP METHOD

- COMPONENT DEPRECiATiON METHOD

Similar assets

Dissimilar assets

working together

Combining several assets for

depreciation (US GAAP)

PAS 16

Single asset - components with

useful life that vary widely.

Separate depreciation for each

major component

E. ADDiTiONAL ASSET - REViSE THE DEPRECiATiON RATE F. COMPOSiTE LiFE - TOTAL DEPRECiABLE AMT ANNUAL DEPRECiATiON

More of straight-

line method

PPE COST RV DA UL

A 260k 20k 240k 6yrs

B 1.5M 300k 1.2M 10yrs

C 870k 70k 800k 5yrs

2,630k 2.240k

GROUP & COMPOSiTE

Annual dep

Depreciation rate

Composite life

2,240,000/320,000 = 7 years

SALE OF PPE C: NO GAiN OR LOSS

Charged to accumulated depreciation

A. PER ASSET BASiS - COMPUTE FOR ANNUAL DEPRECiATiON B. TOTAL THE ANNUAL DEPRECiATiON COMPUTED iN A PER ASSET BASiS C. COMPUTE FOR THE DEPRECiATiON RATE: D. DEPRECiATiON CHARGE =

GROUP & COMPOSiTE

TOTAL ANNUAL DEPRECiATiON TOTAL COST OF ASSETS iN THE GROUP DEPRECiATiON RATE X TOTAL COST OF THE GROUP

Cash 200,

Accum dep 470,

PPE C 870,

Simplification of

bookkeeping. Not

under IFRS

COMPONENT DEPRECiATiON

AiRCRAFT = P50M Split to major components

Body 25M 20yrs 1.25M

Engines 15M 10yrs 1.5M

Internal fittings 5M 5yrs 1M

All others 5M 4yrs 1.25M

5M